The Fundraising Difficulty Curve Nobody Talks About. (Every Founder Gets This Wrong.)

Series A Is Easy. Series B Will Break You.

Ask a first-time founder which round is the hardest to raise, and they’ll almost always say Series A.

They’re wrong.

Ask a founder who’s been through the entire cycle — pre-seed to Series C and beyond — and you’ll get a very different answer. Because the difficulty curve of fundraising isn’t a straight line that gets harder as you go up. It’s a U-shape. And the two hardest points are the ones nobody warns you about.

Here’s the actual difficulty ranking, from easiest to hardest — based on what’s really happening in 2026, not what the textbooks say.

📣 JUST LAUNCHED: DeckSend by Fundreef. Stop attaching your pitch deck to emails. Send it through DeckSend and see exactly who opened it, which slides they read, and how long they spent on each one.

Hundreds of founders are already using it in the first hours since launch. Don’t be the last one still sending decks as attachments.

The Ranking

From easiest to hardest:

Series A — the easiest

Seed — hard but logical

Series C and beyond — a different game

Pre-Seed — brutal

Series B — the hardest round in venture capital

Yes, you read that right. Series A is the easiest. Series B is the hardest. And pre-seed, the round most founders treat as a formality, is now one of the most punishing stages in the entire fundraising journey.

Let me explain each one.

Series A — The Sweet Spot

Difficulty: 4/10

This will surprise most founders. But think about what’s actually true at the Series A stage:

You’ve already survived. You made it through pre-seed and seed — the two stages where most startups die. The mere fact that you’re still alive, still growing, still have a team, already puts you in the top 10-15% of startups that ever raised a seed round. That survival is itself a signal.

You have traction — but nobody expects perfection. At Series A, investors want to see product-market fit signals. Not dominance. Not $10M ARR. Just clear evidence that something is working: growing revenue, strong retention, a repeatable acquisition channel. The bar is real but achievable.

You can still tell stories. This is the crucial part. At Series A, you’re selling a trajectory. “Here’s what we’ve proven. Here’s what we’ll do with $8M. Here’s why this becomes a $100M business.” The investor is buying potential validated by early proof — not certainty. There’s still room for narrative, for vision, for the founder’s conviction to carry weight.

The investor pool is massive. There are more funds writing Series A checks than at any other stage. Every major VC firm has a Series A practice. The competition for deals is intense — which means if your metrics are decent and your story is strong, multiple firms will want to talk to you.

The pattern matching works in your favor. VCs have clear mental models for what a Series A company looks like. If you fit the pattern — $1-2M ARR, 15-20% month-over-month growth, strong retention, a large market — the conversation is straightforward. There’s a playbook. Both sides know it.

This doesn’t mean Series A is easy. It means the rules are clear, the investor pool is deep, and the bar — while real — is the most well-defined of any stage.

Seed — Hard But Logical

Difficulty: 6/10

The seed round is harder than Series A because you have less proof. But it follows a logical framework that founders can prepare for.

At seed, investors want to see: a working product (not just an idea), early user signals (not necessarily revenue), a credible team, and a large enough market to justify the bet.

The challenge is that you’re still mostly selling a hypothesis. But unlike pre-seed, you have something to show. An MVP. Beta users. A waitlist. Design partners. Letter of Intent from a potential customer.

The seed ecosystem is also well-developed. There are hundreds of seed funds, angel syndicates, and accelerator programs designed specifically for this stage. The infrastructure exists. The playbook exists.

What makes seed hard — but not brutal — is that investors know what they’re buying: risk. They’re pricing it accordingly. A $3-5M valuation at seed reflects the uncertainty. Nobody expects you to have it all figured out.

Seed is hard work, but it’s honest work. The rules make sense.

Series C and Beyond — A Different Game

Difficulty: 6/10

By Series C, you’re no longer in “startup fundraising.” You’re in growth equity and pre-IPO territory.

The difficulty here isn’t about convincing someone your company is real. It obviously is — you have tens of millions in revenue, hundreds of employees, established customers. The difficulty is about valuation, terms, and strategic positioning.

The investors at this stage — growth equity firms, crossover funds, sovereign wealth — are running financial models, not making gut bets. They care about revenue multiples, margin profiles, path to profitability, and exit scenarios.

It’s hard in the way that negotiating a complex financial transaction is hard. But it’s not existential. Your company exists. The question is just: at what price, on what terms, and with whom.

I’m not going to spend more time here because most of you reading this aren’t at Series C. The two stages that matter most — and that nobody prepares you for — are the extremes.

Pre-Seed — The New Gauntlet

Difficulty: 8/10

Five years ago, pre-seed was the easiest round to raise. You had an idea, a pitch deck, maybe a prototype. You told a compelling story over coffee. An angel or a small fund wrote you a $200-500K check on conviction alone.

That world is dead.

In 2026, pre-seed has become one of the most punishing stages in fundraising. Here’s why:

A good MVP is no longer enough. The cost of building an MVP has collapsed thanks to AI, no-code tools, and cheap development resources. Every investor’s inbox is full of founders with functional MVPs. Having a working product used to be a differentiator. Now it’s table stakes. It gets you in the door, but it doesn’t get you a check.

Investors want traction before you’ve had time to build traction. The paradox of pre-seed in 2026: you’re raising your first round, but investors want to see paying customers, a waitlist, LOIs, or revenue. “Come back when you have traction” is the most common rejection — but you need the money to build the traction. It’s a chicken-and-egg problem that kills great companies.

The small angel is gone. As we covered in a previous newsletter, the $2K-$10K angel check has largely disappeared. The individual investors who used to fund pre-seed rounds have moved their risk capital to crypto, options, and public market alternatives with better liquidity. The capital pool for tiny first checks has structurally shrunk.

The bar keeps rising. Five years ago: “We have an idea and a deck” → funded. Three years ago: “We have an MVP” → funded. Today: “We have an MVP, 50 beta users, $3K MRR, and a signed LOI from an enterprise customer” → maybe funded. The goalposts have moved dramatically, and most first-time founders don’t realize it until they’ve been rejected 40 times.

Nobody teaches you how to do this. There’s no YC playbook for pre-seed. No established framework. No “here’s what good looks like.” Every fund has different criteria. Some want revenue. Some want team pedigree. Some want a big market. Some want all three. The rules are invisible, inconsistent, and constantly changing.

Pre-seed in 2026 is the stage where the most promising founders get stuck — not because their ideas are bad, but because the infrastructure to fund very early companies has hollowed out while the expectations have inflated.

Series B — The Hardest Round in Venture Capital

Difficulty: 10/10

If pre-seed is a gauntlet, Series B is a firing squad.

Here’s why Series B is, by far, the most difficult round to raise — and the one that breaks the most promising companies:

They treat you like a public company. You’re still a startup.

At Series A, you’re selling a story backed by early traction. At Series B, the story is over. Investors want hard numbers. Revenue growth, unit economics, gross margins, net retention, CAC payback periods, LTV:CAC ratios, burn multiple — every metric gets scrutinized with the rigor of a public market analyst.

But here’s the cruel part: you’re still a scrappy startup. You probably have 40-80 employees. Your finance team might be one person and a spreadsheet. Your data infrastructure is held together with duct tape. You’re being evaluated like a Fortune 500 company while operating like a garage band that just got a record deal.

The customers have to be real. And big.

At Series A, you can have a handful of customers and a strong growth trajectory. At Series B, investors want to see: established enterprise relationships, big logos, high net retention, and proof that your sales motion is repeatable, not just lucky.

“We have 10 customers” isn’t enough anymore. “We have 10 customers, 140% net retention, three Fortune 500 logos, and a sales cycle that’s gone from 6 months to 6 weeks” — that’s Series B language. If you don’t have that kind of proof, the conversation doesn’t even start.

The growth has to be enormous AND efficient.

At Series A, growing fast and burning cash is acceptable. At Series B, you need to be growing fast AND showing a path to efficiency. The era of “growth at all costs” is over. Investors want to see that you can scale revenue without scaling burn proportionally.

This is where most Series B companies fail. They grew fast enough to raise an A but haven’t yet figured out the economic model that makes the growth sustainable. And Series B investors — who are writing $20-50M checks — can’t afford to bet on “we’ll figure out unit economics later.”

The investor pool is surprisingly small.

This is counterintuitive. You’d think more money would be available as you move up. But the number of firms that actively write Series B checks is actually smaller than the number writing Series A checks. Many early-stage funds stop at A. Many growth funds don’t start until C. Series B sits in an awkward middle ground where fewer specialized investors play.

The failure rate is devastating.

Here’s the stat that should scare every founder: a significant percentage of companies that raise a Series A never raise a Series B. They don’t all die — some get acquired, some become profitable, some pivot. But many simply can’t make the jump from “promising early-stage company” to “proven growth-stage company.”

The gap between Series A and Series B is the widest chasm in the entire fundraising journey. And most founders don’t see it coming because they’re still celebrating the A.

The emotional toll is the worst.

At pre-seed, rejection is expected. You’re a nobody with an idea. It doesn’t feel personal.

At Series B, you’ve been building for 3-4 years. You have a team that depends on you. You have customers who trust you. You’ve raised $10-15M already. And now an investor is telling you: your growth isn’t fast enough, your margins are too thin, your market position isn’t clear.

That hits different. Series B rejection isn’t “your idea is too early.” It’s “your execution isn’t good enough.” That’s a much harder thing to hear — and a much harder thing to fix.

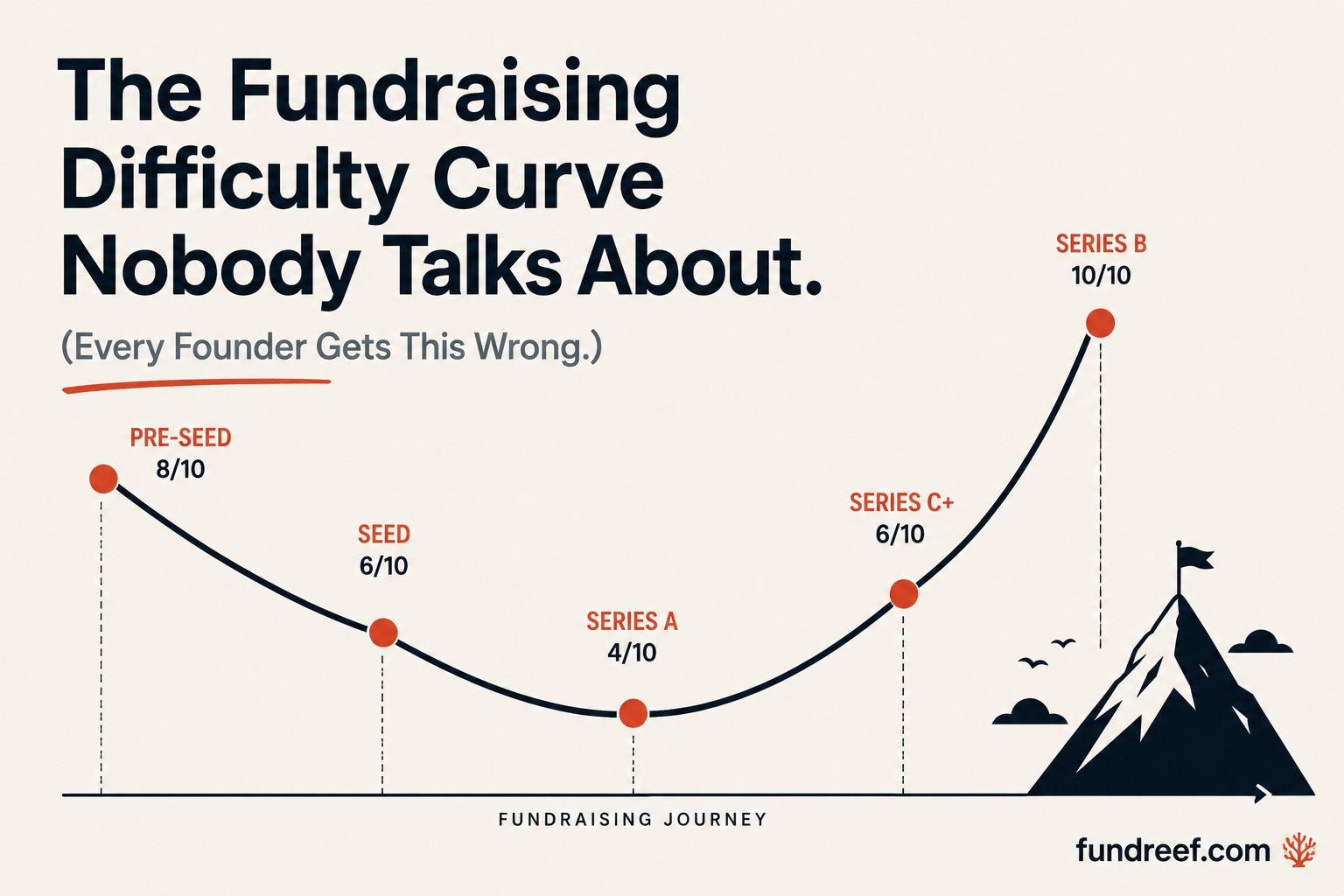

The Difficulty Curve

If you map it visually, the fundraising difficulty curve looks like this:

Pre-Seed → Seed → Series A → Series B (8/10) → (6/10) → (4/10) → (10/10)

It drops in the middle and spikes at the end. The two extremes — the very beginning and the transition to growth stage — are where companies die.

Series A is the eye of the storm. Enjoy it while it lasts.

What This Means for You

If you’re at pre-seed: Don’t walk in with just an MVP. Have traction — any traction. Revenue, users, LOIs, partnerships. The bar has moved. Accept it and over-prepare.

If you’re approaching Series A: This is your moment. The rules are clearest here, the investor pool is deepest, and the bar — while real — is achievable. Don’t overthink it. Hit the metrics, tell the story, run a tight process.

If you’re between A and B: Start preparing for Series B the day you close your A. Not three months before you need to raise. Build the data infrastructure, the finance function, the customer case studies, and the unit economics now. Because by the time you need them, it’s too late to build them.

If you’re at Series B: You already know how hard this is. The only advice worth giving: don’t try to fake the numbers. Series B investors have seen it all. Authenticity and a clear-eyed view of your challenges will serve you better than a polished deck hiding weak metrics.

The Uncomfortable Truth

The fundraising journey isn’t a ladder where each step is slightly harder than the last. It’s a rollercoaster with two valleys that swallow companies whole.

Most founders prepare for the wrong round. They stress about Series A — which is actually the most navigable stage — and walk blindly into pre-seed and Series B, which are the two stages most likely to kill them.

Now you know the curve. Plan accordingly.

Wherever you are on the curve, find the right investors for your stage. Fundreef indexes 500,000+ investors by stage, sector, ticket size, and geography — from pre-seed specialists to growth equity firms.

→ Find Your Investors on Fundreef

Fundreef is the AI-powered fundraising suite for startup founders. Investor database, pitch deck tools, AI valuation, and DeckSend — everything you need to close your round.

Great post! I'm curious—what do you think is the biggest misconception founders have about the fundraising process? It seems like many underestimate the emotional rollercoaster involved. Would love to hear your thoughts on navigating that!

we tracked this data in our daily yesterday too so it's interesting to see how your cut differs. the seed to A gap is quite steep nowadays